Money rarely creates tension because of math. It creates tension because of ambiguity. When couples say finances feel stressful, the issue is often unclear expectations rather than insufficient income.

One partner assumes something is covered. The other assumes it is not. Shared expenses mix with personal purchases. Savings goals float without structure. Small questions turn into recurring conversations. Clarity reduces conflict.

The three-account money setup is not complicated, but it creates boundaries inside your finances that make decision-making easier. It protects shared responsibility while preserving individual autonomy. It reduces the need for constant permission-based spending discussions.

Most importantly, it gives your money a visible structure that both partners understand. This approach works well for couples at many stages, from newlyweds combining accounts for the first time to long-term partners who want less friction around spending.

Why Shared Finances Often Feel Confusing

Many couples default to one of two extremes. Some combine everything into one account and assume shared transparency will solve confusion. Others keep everything separate and split bills informally each month. Both methods can work, but both leave room for frustration.

With one fully combined account, small personal purchases can feel scrutinized. Even if neither partner intends judgment, visibility can create tension. With fully separate accounts, shared expenses may feel uneven or require frequent transfers and calculations.

The issue is not whether money is shared. The issue is whether roles and flows are clear. When structure is missing, conversations about money happen reactively. When structure is present, most decisions become automatic.

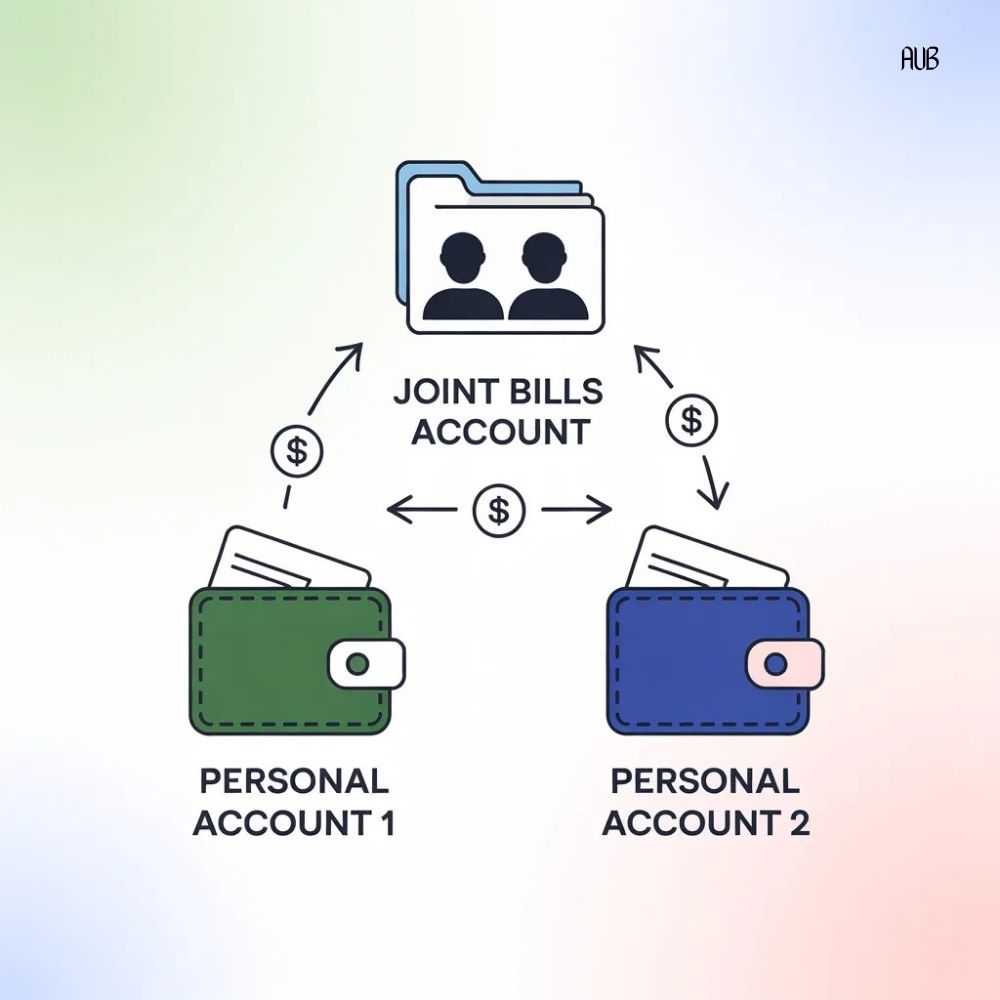

The Three-Account Framework Explained

The three-account setup consists of:

- One Joint Bills Account

- Two Personal Accounts

This does not require opening three entirely new banks. In many cases, couples already have individual accounts and simply need to create one shared account specifically for household expenses.

The design is simple. All shared obligations flow through one place. Personal spending remains separate and autonomous. Let’s break down each piece clearly.

Account One: The Joint Bills Account

This account exists solely for shared financial responsibilities. It is not for casual spending, and it is not for personal purchases.

Typical expenses that belong in this account include:

- Rent or mortgage

- Utilities

- Insurance

- Groceries

- Child-related expenses

- Subscriptions used by both partners

- Savings contributions for shared goals

Each partner contributes a predetermined amount into this account every month. The contribution can be equal or proportional to income, depending on what feels fair and sustainable.

For example, if both partners earn similar incomes, they may contribute equal amounts. If one partner earns significantly more, a proportional contribution often feels more balanced. The critical element is that the number is decided intentionally, not improvised monthly.

Once money enters the joint account, it is designated for shared priorities. Bills are automated whenever possible to reduce manual oversight.

This creates clarity. Both partners know what shared life costs. Both partners know that those costs are covered.

Account Two and Three: Personal Autonomy Accounts

Each partner keeps a personal account separate from the joint account. After contributing to the joint account, the remaining income stays in their individual account for personal spending, hobbies, clothing, gifts, and discretionary purchases. This autonomy reduces friction significantly.

If one partner wants to purchase a new gadget, update their wardrobe, or invest in a personal interest, they can do so without negotiation, as long as shared obligations are already funded.

Personal accounts eliminate the feeling of financial surveillance. They also reduce resentment that can arise when one partner feels their spending is constantly observed or questioned. Autonomy inside structure is the key advantage of this system.

How to Decide Contribution Amounts

This step requires one intentional conversation. Start by calculating total shared monthly expenses, including fixed bills and average variable costs such as groceries and utilities. Add a buffer for unexpected expenses. Then divide that total based on your agreed-upon method.

For example, if shared expenses total $4,000 per month and both partners earn similar incomes, each might contribute $2,000 into the joint account.

If income is uneven, you might calculate percentage contributions. If one partner earns 60 percent of total household income and the other earns 40 percent, contributions may reflect that ratio.

The goal is not rigid equality. The goal is perceived fairness. Once the contribution number is set, automate transfers on payday. This prevents monthly renegotiation.

Adding a Shared Savings Layer

Within the joint account or as a fourth linked savings account, you may create shared savings categories such as:

- Emergency fund

- Vacation fund

- Home improvement fund

- Annual insurance payments

You can keep these savings physically separate for clarity or track them through labeled sub-accounts. This step strengthens long-term planning and prevents savings from blending with daily spending.

Common Concerns and How to Address Them

Some couples worry that separating personal spending reduces transparency. In practice, the opposite is often true.

Transparency improves when shared obligations are centralized. Personal spending becomes less threatening because it no longer affects household stability.

Another concern is income fluctuation. If one partner’s income changes temporarily, revisit contribution percentages rather than abandoning the structure entirely. The system should adapt to life changes, not collapse under them.

The Long-Term Benefits

Over time, this system builds several important habits.

- It strengthens financial awareness because both partners see shared costs clearly.

- It protects autonomy, which reduces resentment.

- It creates predictability, which lowers anxiety.

- It makes future planning easier because savings are intentional rather than accidental.

Money becomes a shared project rather than a recurring debate.

Why Simplicity Works Better Than Complexity

There are many financial models available to couples. Some are detailed, spreadsheet-heavy systems with multiple categories and tracking tools. While those can be effective, they often fail because they are difficult to maintain.

The three-account setup works because it is simple enough to sustain. When structure is clear, conversations become shorter and calmer.

And in long-term partnerships, reducing friction around everyday systems is one of the most practical ways to strengthen stability. Money will always require attention. With the right structure, it does not need to require tension.